Close Cookie Popup

Cookie Settings

By clicking “Accept”, you agree to the storing of cookies on your device to improve our services and your browsing experience.

From 2026 onwards, packaging compliance in the UK and Europe stops being a future problem and becomes a live operational issue for brands, particularly those using flexible packaging. Two regulatory regimes are driving this shift.

In the United Kingdom, Extended Producer Responsibility (EPR) is moving from theory to cash, with confirmed fees, growing eco-modulation, and increasing pressure from finance teams on packaging decisions.

In the European Union, the Packaging and Packaging Waste Regulation (PPWR) introduces a single EU-wide framework combining design rules, market-access requirements, and EPR obligations under one umbrella

These systems are related but not interchangeable. Understanding the nuance of each is critical for any brand operating in the region.

The UK and EU are solving similar problems in different ways. Both regimes aim to shift waste costs back to producers, improve recyclability and real-world outcomes, and force better packaging data and governance. But they do it through very different levers.

In the EU, PPWR is the top-level rulebook. It sets what packaging is permitted to be placed on the EU market, defines recyclability, labelling, minimisation, reuse, and recycled-content requirements, and embeds EPR as the funding mechanism for waste management once packaging has passed those design tests. Packaging must first pass PPWR design requirements. Only then does EPR apply. Paying higher EPR fees does not make non-compliant packaging compliant.

The UK does not have a PPWR-equivalent market-access regulation. UK packaging compliance is driven through EPR registration, detailed data reporting, and fees increasingly modulated by recyclability. In the UK, most packaging can still be sold but some formats will cost materially more to put on the market. This distinction is the most important thing to understand before making packaging decisions for either market.

Under UK EPR, a “producer” may be the brand owner, the importer, the packer/filler, or the seller of packaged goods into the UK market. For most mid-to-large brands: mandatory registration, full data reporting, and liability for waste-management fees.

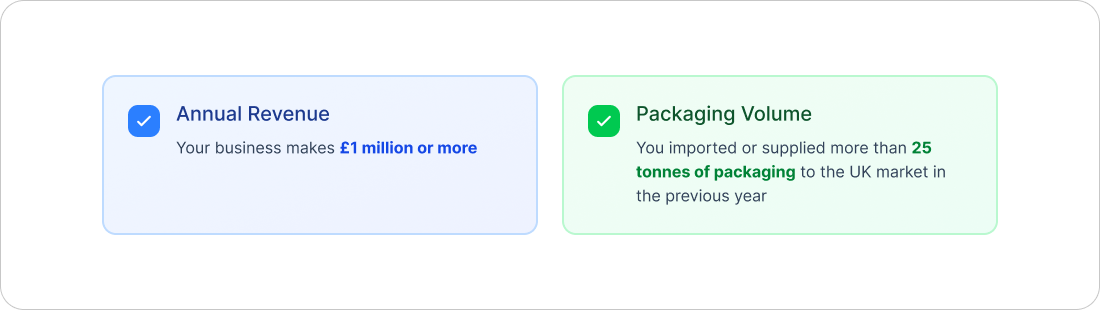

Large producer: Turnover ≥2m AND >50 tonnes packaging handled. Reports twice yearly. Pays EPR waste management fees.

Small producer: £1m-£2m AND >25t, OR >£1m AND 25-50t. Reports annually. Not currently paying EPR fees (under review).

Note: corporate group thresholds apply at group level.

UK EPR reporting requires granular packaging data: material type, format, weight, and whether packaging is household or non-household. For flexible packaging, common problem areas include:

From 2026 onwards, poor data creates direct financial exposure through incorrect fee calculation, audit vulnerability, and inability to defend packaging decisions under regulatory scrutiny.

First invoices: October 2025 (large producers), calculated from 2024 calendar year volumes.

Payment options: 50 days, or quarterly installments (Nov 2025, Jan 2026, Apr 2026, Jun 2026 at 25% each).

Warning: an October 2025 invoice can feel like a sudden hit if liability was not accrued as volumes were sold.

EPR fees fund local authority waste management. PRNs remain the mechanism for meeting recycling targets. Large producers must still buy PRNs and PERNs. PRN pricing is volatile, especially plastics. Your total compliance cost exposure can swing due to PRN market dynamics even with robust EPR fee modelling.

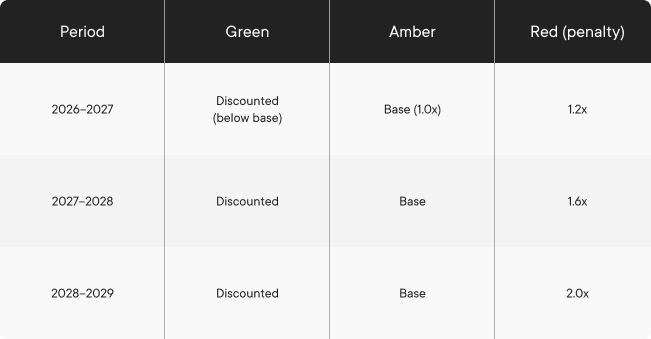

From 2026, UK EPR links cost to recyclability through modulated fees. Packaging is rated via the Recyclability Assessment Methodology (RAM):

Example (plastic): Base fee £423/tonne. Red 2026 at 1.2x = £507.60. Red 2028 at 2.0x = £846.

For plastics:

For paper and board:

For glass:

The PPWR framework applies from 12 August 2026. This means PPWR becomes the default design baseline for EU packaging, and packaging decisions made in 2026–2027 must anticipate later requirements.

For brands using flexible packaging, the most material additions are:

None of these obligations are resolved by paying higher EPR fees. They require packaging design decisions to be correct from the outset.

Under PPWR, brands must maintain technical documentation demonstrating compliance. For flexible packaging, this typically includes:

This documentation is what protects brands during audits, enforcement actions, and retailer compliance challenges, all of which are becoming more frequent. Brands that cannot produce it on request face exposure that goes well beyond a fee adjustment.

For brands in both markets: design to EU PPWR standards, model UK EPR costs separately.

For brands selling into both markets: design to the stricter direction of travel (EU PPWR) while modelling UK EPR costs separately to understand the financial impact of specific format choices. The cost of redesigning at scale under time pressure is consistently higher than the cost of designing correctly now.

What is the difference between UK EPR and EU PPWR?UK EPR is a cost-allocation mechanism: packaging remains legal to sell but attracts fees based on recyclability performance. EU PPWR is a market-access regulation: packaging must meet design and recyclability requirements before it can legally be placed on the EU market. Poor recyclability under UK EPR costs you money. Non-compliance under EU PPWR can prevent you from selling at all.

The PPWR framework applies from 12 August 2026. Not all obligations activate immediately, but it becomes the default design baseline from that date.

Generally yes. Multi-layer laminates and formats with weak real-world recycling pathways typically attract higher fees under eco-modulated EPR. Mono-material PE or PP structures with PCR content attract lower fees. Kerbside collection for flexible packaging is planned within the next 12 to 24 months in the UK, which will improve classifications over time.

Not automatically. A format that is legal and cost-manageable under UK EPR may still fail EU PPWR design or recyclability requirements. Brands in both markets should design to EU PPWR standards and model UK EPR costs separately.

.png)