Close Cookie Popup

Cookie Settings

By clicking “Accept”, you agree to the storing of cookies on your device to improve our services and your browsing experience.

The US does not yet have a single national EPR framework. What it has is a fast-moving, state-by-state patchwork already creating real compliance obligations, real deadlines, and real fee exposure for brands placing packaging on the market. For flexible packaging specifically — stand-up pouches, multi-layer films, laminate structures — the stakes are particularly high. Brands that don’t adapt their formats are looking at a potential 15 to 40 percent increase in total packaging spend. That figure alone should be driving urgency.

Extended Producer Responsibility shifts the financial burden of managing packaging waste away from municipalities and onto the producers who put that packaging into the market, in most cases, brand owners.

For flexible packaging, this shift is significant. Multi-layer films and non-recyclable laminates have historically been difficult to sort and recycle, and EPR schemes are designed to reflect that through fees and eco-modulation. Flexible packaging structures that cannot be cleanly recycled in existing infrastructure often sit in the highest fee brackets. The practical result is that EPR acts as a price signal, pushing brands toward mono-material films or fibre-based alternatives by making the cost of staying with complex laminates increasingly visible on the balance sheet.

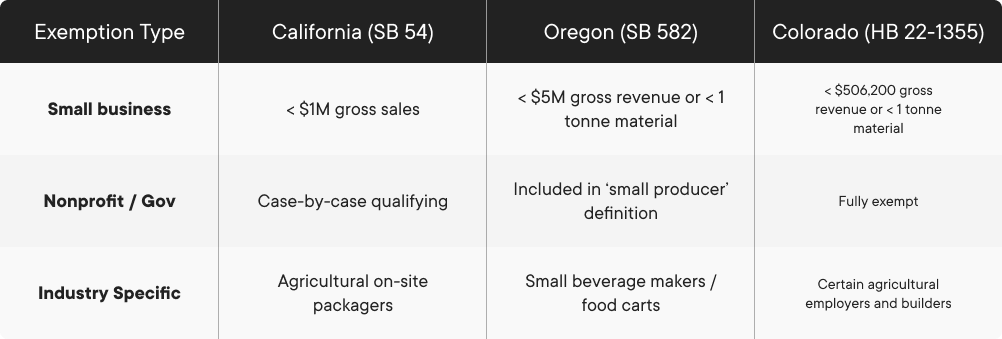

The Circular Action Alliance (CAA) has been selected as the PRO across every currently active US programme. This means brands operating across multiple states have a single point of registration, rather than managing separate relationships with each state authority. It does not, however, eliminate the complexity of meeting each state’s individual reporting requirements, which vary considerably in detail and structure.

Liability under US EPR laws generally falls on the brand owner, provided they have a US presence. For flexible packaging, this plays out in specific ways:

Reporting under US EPR schemes is more granular than most brands expect. You cannot simply report “a pouch.” Reporting requires a component-level breakdown of everything that makes up that pack.

This level of detail requires accurate packaging specifications, not estimates. Brands that don’t have component-level data documented internally will need to work with their packaging suppliers before reporting deadlines arrive.

Fees are assessed per pound of packaging placed on the market. Because flexible packaging is lightweight, the per-unit fee on any single pack may appear modest. But the per-pound rate for multi-layer plastics is substantially higher than for paper or rigid mono-materials, and those rates compound quickly at volume.

Early modelling from Oregon: flexible films are projected to be assessed at $0.54 to $1.43 per pound, compared to roughly $0.03 per pound for corrugated cardboard. That is a cost difference of up to 47 times for the same weight of material.

Fee exposure is not fixed. Packaging design decisions directly determine what brands pay. Four practical levers:

EPR schemes heavily favour recyclable materials, which can create pressure to move from lightweight flexible pouches toward heavier rigid plastic or glass formats. In some cases, this shift does lower the fee rate per pound, but it simultaneously increases total packaging weight, total material cost, overall carbon footprint, and shipping costs. A decision that looks favourable on the EPR fee sheet can quietly erode margin and sustainability credentials elsewhere.

Format transitions need to be modelled across the full cost picture, including EPR fees, material costs, weight, freight, and carbon, before committing. Optimising for one variable in isolation creates unintended consequences across the others.

The combination of live deadlines, granular reporting requirements, and significant fee exposure for flexible packaging formats means a “wait and see” approach carries real cost. Brands that audit their packaging specifications now, understand their fee exposure by state, and begin format transitions where the case is clear will be in a materially better position than those treating this as a compliance task to manage at the last minute.

EPR fees are a design input, not an afterthought. The sooner they are treated as such, the more options a brand has.

Oregon, California, Colorado, and Washington have the most advanced programmes, with key deadlines landing in 2026. Maryland, Maine, and Minnesota are also in active implementation. More states are expected to follow within the next two to three years.

Yes, and flexible packaging is often in the highest fee brackets. Multi-layer laminates and non-recyclable film structures are treated less favourably than mono-material or fibre-based alternatives under most state frameworks.

Fees are assessed per pound of packaging placed on market. Multi-layer plastics typically attract significantly higher per-pound rates than paper or mono-material plastics. Early Oregon modelling suggests flexible films could be assessed at $0.54 to $1.43 per pound, compared to approximately $0.03 per pound for corrugated cardboard.

Switching from lightweight flexible packaging to heavier rigid formats can lower your EPR fee rate per pound but increase total material cost, weight, carbon footprint, and shipping costs. Fee rate and total cost are not the same thing, and format decisions should be modelled across all variables before committing.