Close Cookie Popup

Cookie Settings

By clicking “Accept”, you agree to the storing of cookies on your device to improve our services and your browsing experience.

Extended producer responsibility (EPR) laws are no longer on the horizon. In Oregon and Colorado, fees are already being collected. In the EU, the Packaging and Packaging Waste Regulation (PPWR) entered into force in February 2025, with binding obligations from August 2026. In the UK, the EPR scheme went live in 2025. In California, the programme launches in 2027.

For brand owners, the question has shifted. It is no longer "will we have to comply?" It is "how much will compliance cost, and what does it cost our competitors?"

Those are two very different questions. The answer to the second one is where your competitive opportunity sits.

READ MORE: Our EPR 101 Guide linked here

Packaging regulation is moving the same way across every major market. The mechanisms differ by jurisdiction, but the underlying logic is the same: the polluter pays principle. Brands that create packaging are being made financially responsible for what happens to it at end of life.

The PPWR is the most comprehensive packaging reform in a generation. Its first binding obligations apply from 12 August 2026, with requirements escalating through 2030 and beyond.

The regulation operates across three levers:

By 2030, all packaging placed on the EU market must be recyclable. Minimum recycled content thresholds apply to plastic packaging from 2030, varying by packaging type: 35% for non-contact plastic packaging, 25% for single-use plastic beverage bottles, with targets rising in subsequent years.

The PPWR also harmonises EPR across all 27 EU member states. For brands selling into multiple European markets, the practical effect is a single regulatory baseline pushing packaging design toward recyclability and minimum plastic use.

READ MORE: You can dive deep into our PPWR guide here

There is no federal US packaging EPR law. Seven states have enacted their own programmes, with Oregon and Colorado already collecting fees.

BCG's 2025 analysis of North American packaging identifies state-level EPR as one of three potential accelerants for a broader industry sustainability tipping point. If large states continue to legislate, brands will face the choice of reformulating packaging or managing immense operational complexity selling different product variants across different states. The trajectory is clear even if the pace is uncertain.

Oregon illustrates what is at stake. First-cycle fees ranged from $0.08 to $0.77 per pound of covered material, a roughly ten-fold difference driven by material type and eco-modulation score. A brand placing significant volumes of non-recyclable flexible film on the Oregon market faces a materially different fee liability than a brand with corrugated or uncoated paper packaging at the same volume.

The UK's EPR scheme for packaging went live in 2025, requiring brand owners and importers to register with a Producer Responsibility Organisation (PRO), report packaging data, and pay fees based on material type and weight. The UK scheme uses eco-modulation: formats accepted in kerbside recycling attract the lowest fees; formats that are not accepted attract higher ones.

For brands operating across the UK and EU simultaneously, packaging design decisions now carry direct financial consequences in multiple markets at once.

READ MORE: You can read our updates on UK EPR here.

EPR changes the cost structure of packaging in a way that favours brands with more recyclable formats. That is not a side effect. It is the mechanism by which EPR is designed to drive packaging redesign at scale.

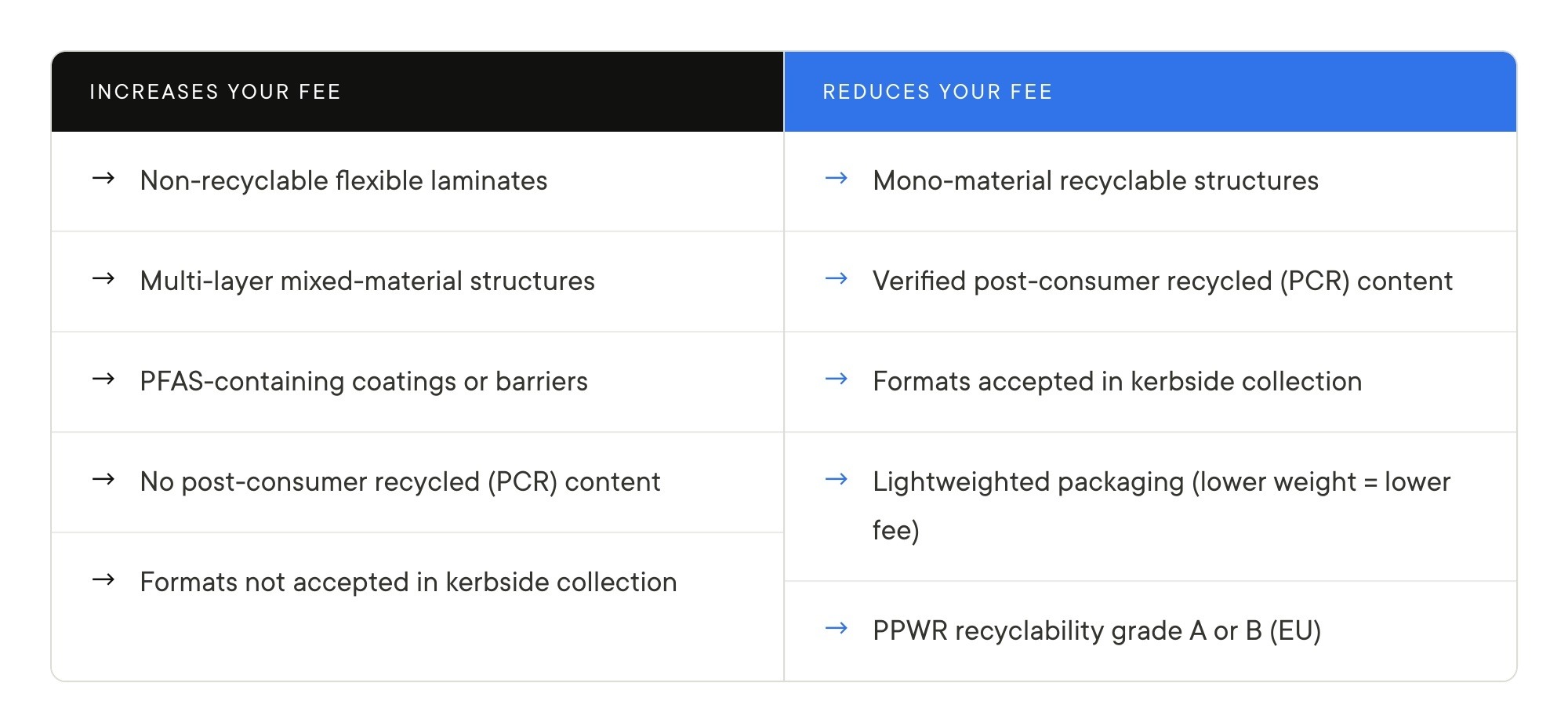

Two brands selling comparable products in comparable volumes can face very different fee obligations depending on what their packaging is made of. A brand using multi-layer flexible laminates pays more. A brand that has already switched to mono-material structures, certified compostable films, or fibre-based alternatives pays less. That difference compounds across multiple markets and multiple fee cycles.

This is what makes EPR a competitive issue, not just a compliance issue. The brands that have already invested in packaging redesign will build a structural cost advantage over those that have not. Lower fees in Oregon. Lower fees in Colorado. Lower fees in California. Lower compliance costs across the UK and EU. The fee differential is not a one-off. It compounds every reporting cycle.

BCG's North American packaging analysis confirms this dynamic. Paper and recyclable mono-material flexible plastic are emerging as the material categories with the strongest tailwinds. Brands that have made those transitions are building resilience into their packaging portfolios, not just meeting compliance requirements.

EY's 2025 PPWR strategy briefing puts it plainly: "Reducing packaging and improving recyclability can deliver significant fee reductions at portfolio level. Use eco-modulation systems and follow the most advanced rules as a proxy for future EU harmonisation to guide portfolio redesign."

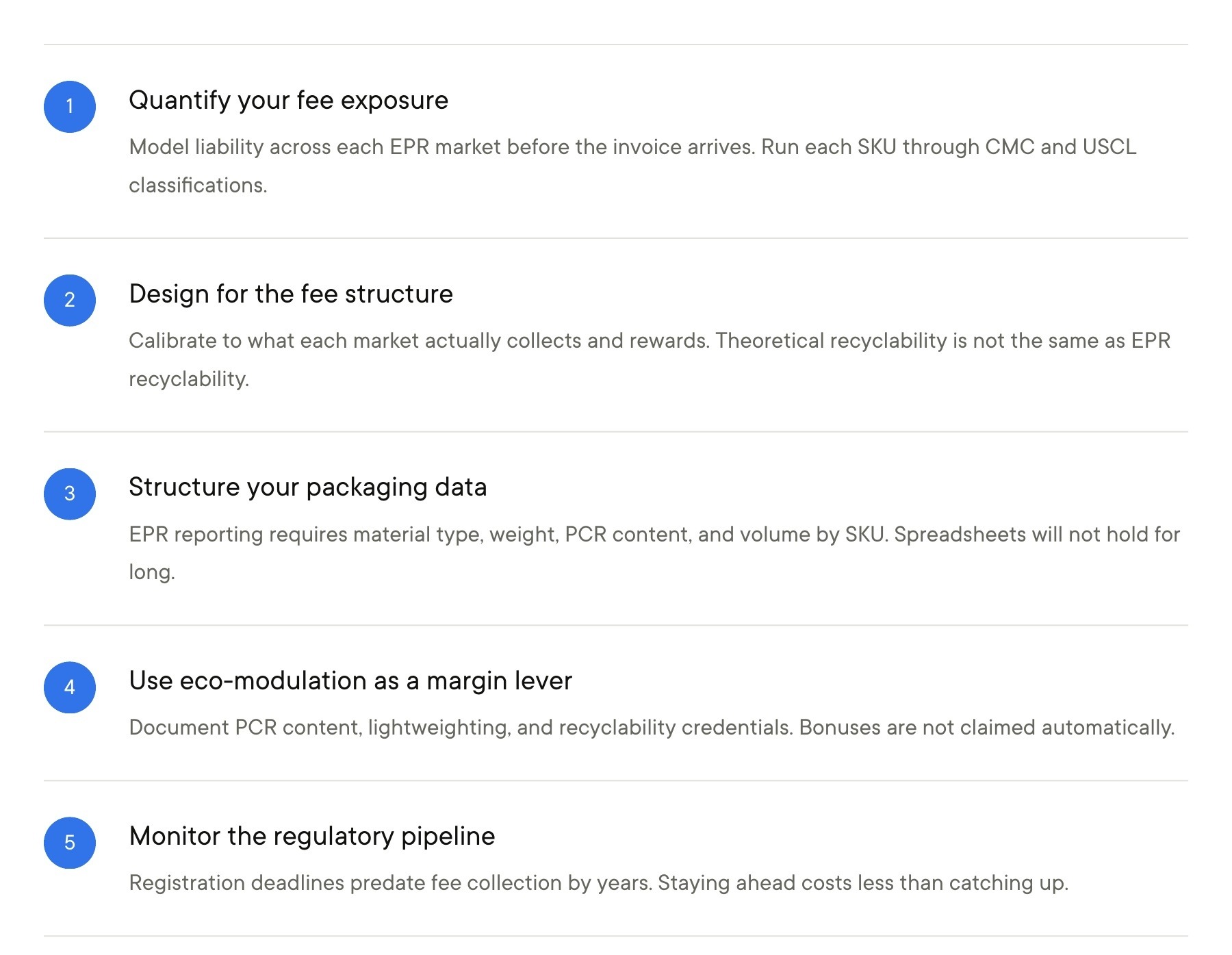

Until you have modelled your current fee liability across each active EPR market, you are managing compliance without a cost model.

The business case: Fee modelling turns packaging redesign from a brand decision into a financial calculation with a provable ROI.

Recyclability under EPR is defined by what is actually collected, sorted, and sold into functioning end markets in each jurisdiction, not by what is technically recyclable. Most flexible packaging formats fail this test today.

Design choices need to be calibrated against what each market's EPR programme actually rewards:

The practical design changes that move you down the fee curve in most markets:

None of these is cost-free. Each involves trade-offs between barrier performance, unit economics, and fee position. Quantifying your fee exposure first turns those trade-offs into a financial calculation you can actually make.

EY's 2025 analysis found that 73% of companies still rely on manual spreadsheets for sustainability data. That is not a viable position for EPR compliance. Reporting to the CAA or a UK PRO requires material type, weight, PCR content percentage, recyclability classification, and volume by market, broken down by packaging component.

Steps to close the data gap:

The business case: Brands with clean packaging data can model fee positions across multiple EPR scenarios, identify eco-modulation bonuses faster, and respond to rule changes by finding affected SKUs immediately rather than rebuilding data from scratch each cycle.

Every active EPR programme adjusts base fees up or down based on packaging performance. Recyclable formats attract credits. Non-recyclable formats attract penalties. PCR content is rewarded. PFAS-containing coatings are penalised.

How eco-modulation works in practice:

If your packaging already includes verified PCR content, has been lightweighted, or qualifies for a recyclability label, document it and claim the bonus. These are not automatic. You have to report the supporting data. Brands that do will systematically pay less than competitors with equivalent packaging who do not file the documentation.

The regulatory environment is moving faster than most brands' packaging review cycles. PPWR delegated acts are still being finalised. US state programmes have registration deadlines that predate fee collection by years.

A practical monitoring framework:

The business case: Brands that engage ahead of regulatory timelines can design packaging for future compliance while current stock is still being used. Brands that wait for fee invoices have no such flexibility, and the cost of catching up is higher than the cost of staying current.

EPR compliance is a data problem before it is a design problem. You cannot calculate your fee exposure, claim eco-modulation bonuses, or report accurately without reliable packaging data. The EY finding that 73% of companies are managing this with manual spreadsheets suggests most brands are significantly underprepared for the reporting requirements they are already subject to, and for the additional ones coming in California, Minnesota, Maryland, and Washington.

Building clean packaging data infrastructure is a one-time investment that serves every compliance cycle that follows:

The brands with this infrastructure can model fee positions across multiple EPR scenarios before committing to a redesign. The brands rebuilding data from scratch each reporting cycle cannot.

For brands selling into multiple EPR markets simultaneously, the financial logic of packaging redesign is stronger than any single-market calculation suggests. A switch from a multi-layer flexible laminate to a mono-material or fibre-based structure reduces fee exposure in Oregon, Colorado, California, the UK, and across the EU in a single move. The fee saving stacks across programmes.

There is no single packaging format that solves EPR across all seven US states, the UK, and the EU at once. Every format involves trade-offs. But the trade-offs are now financially explicit in a way they were not three years ago. The fee is the price of the current design. The eco-modulation bonus is the financial value of a better one.

BCG frames this as a structural shift: paper and mono-material flexible plastic are the material categories with the most regulatory and commercial tailwinds. The brands investing in this transition now are positioning for lower EPR fees, better recyclability classifications, and more defensible sustainability claims across every market simultaneously.

EPR schemes are designed to favour recyclable materials, and they do. But that incentive can create a trap for brands that optimise narrowly.

The pressure to reduce EPR fees sometimes pushes brands toward heavier rigid plastic or glass formats, on the basis that these attract lower fee rates per pound than lightweight flexible pouches. In some cases that calculation is correct. But a lower fee rate per pound is not the same as a lower total cost.

Switching from a lightweight flexible format to a heavier rigid one typically means:

A format transition that looks favourable on the EPR fee sheet can quietly erode margin and sustainability credentials across every other variable that affects unit economics.

The business case: Any format transition needs to be modelled across the full cost picture before committing: EPR fees, material cost, weight, freight, and carbon. Optimising for one variable in isolation creates unintended consequences across the others. The goal is not the lowest fee rate. It is the lowest total cost of packaging, including what you pay in fees, freight, and materials combined.

EPR is not a temporary regulatory experiment. It is the permanent operating environment for packaging. Oregon and Colorado are collecting fees now. California, the UK, and the EU are building toward full enforcement. The brands that treat this as a design and data strategy will build durable advantages on cost, carbon, and credibility. The brands that treat it as a back-office compliance task will pay for it, literally and repeatedly, across every market they sell into.

The competitive advantage is real. It is quantifiable. It compounds with every fee cycle, across every EPR market. The window to build it ahead of competitors is narrowing.

Grounded works with brands using flexible packaging to navigate EPR compliance, identify fee reduction opportunities, and evaluate packaging redesign options against real market requirements. Get in touch or explore our EPR resources hub for state-by-state and market-by-market guidance.

Yes, in most cases. Every active EPR programme defines producers based on where packaging is placed on the market, not where the brand is headquartered. If you ship packaged goods to consumers in Oregon, California, or the UK, you are a producer in those markets regardless of where your business is registered. E-commerce brands shipping internationally are typically in scope for both product packaging and shipping materials.

Eco-modulation adjusts base EPR fees up or down based on packaging performance. Formats that are recyclable, contain PCR content, or have a lower environmental footprint attract fee credits. Formats that are not recyclable, contain PFAS, or impose costs on waste systems attract fee increases. The result is that two brands with equivalent packaging volumes can face materially different fee obligations depending on what their packaging is made of. That saving repeats every fee cycle across every EPR market they operate in.

The Packaging and Packaging Waste Regulation (PPWR) is the EU's overarching packaging framework, in force from February 2025. EPR is the funding mechanism within it: producers pay for the end-of-life management of the packaging they place on the market. The PPWR goes further than EPR alone. It mandates minimum recycled content in plastic packaging (varying by type from 2030), recyclability requirements for all packaging, and reuse targets in specific format categories. Brands selling into the EU need to comply with the PPWR's design requirements and its fee obligations.

Start with a packaging data audit. List every SKU you sell in Oregon, Colorado, the UK, or the EU, and gather the material composition, weight per unit, and approximate annual volume in each market. Run each SKU through the CMC classification framework for the relevant state. This gives you a fee estimate by SKU, which tells you where your largest exposure sits and where redesign investment would deliver the most fee reduction. Without this model, every compliance and design decision is made without a financial baseline.