June 25, 2026

Scope 1, 2 and 3 Emissions Explained: Where Does Your Packaging Sit?

A company's supply chain emissions are, on average, 5.5 times higher than its direct emissions. For consumer goods brands, Scope 3, the category that captures supply chain impacts, typically accounts for over 80% of total greenhouse gas emissions.

Most brands report Scope 1 and 2 with reasonable confidence. Scope 3 is where the picture gets harder, and where most of the actual footprint lives.

The GHG Protocol: the framework behind the scopes

The Greenhouse Gas Protocol (GHG Protocol) is the world's most widely used standard for measuring and managing greenhouse gas emissions. Virtually every corporate sustainability reporting system is built on it, including CSRD, the Science Based Targets initiative (SBTi), and CDP.

The Protocol's core insight is that a company's full climate impact cannot be measured by looking only at what happens inside its own walls. A brand that outsources manufacturing and uses contract logistics is not a low-emissions company simply because its offices are efficient. Its real climate impact is distributed across its supply chain.

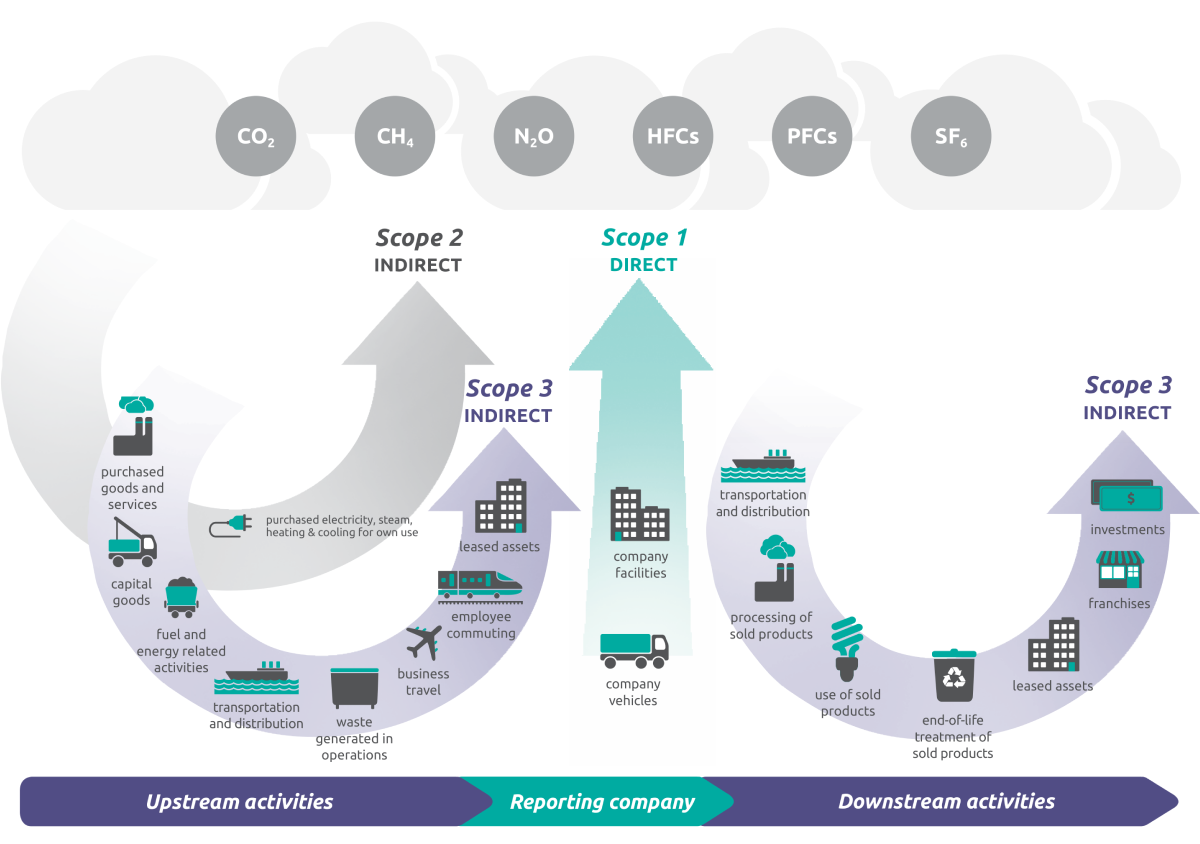

To organise this, the GHG Protocol divides emissions into three scopes based on where they originate and how much control a company has over them.

Source: GHG Protocal

Scope 1: Direct emissions

Scope 1 covers emissions from sources the company directly owns or controls. For most brand owners, this is the smallest scope.

Scope 1 typically includes:

- Any manufacturing processes the brand operates directly on its own sites

- Heating and cooling systems at owned or operated facilities

- Refrigerant gases that leak from company-owned equipment

For brand owners whose operations are primarily office, warehouse, or retail-based, Scope 1 is likely modest relative to the full emissions picture.

Scope 2: Purchased energy emissions

Scope 2 covers the indirect emissions from electricity, heat, steam, or cooling that a company purchases and uses. The company does not generate these emissions directly, but its energy consumption drives them.

The GHG Protocol allows two calculation methods for Scope 2:

- Location-based: uses average grid emissions factors for the region where energy is consumed.

- Market-based: uses emissions factors associated with specific energy contracts, such as renewable energy certificates or Power Purchase Agreements.

For brands that have switched to renewable energy procurement, market-based accounting allows the carbon benefit of those contracts to be reflected in reported emissions. This is why many companies' Scope 2 has declined in recent years even as their operations have grown.

Scope 2 is relatively straightforward to reduce through renewable energy procurement. Most companies tackle it first, before turning attention to the harder problem of Scope 3.

Scope 3: All other indirect emissions

Scope 3 covers all other indirect emissions in the value chain, both upstream from suppliers and downstream through customers and end-of-life. It is the most complex scope, and for most brands, by far the largest.

A company's supply chain emissions are estimated to be, on average, 5.5 times higher than its direct emissions. For consumer goods brands, Scope 3 typically represents over 80% of total greenhouse gas emissions. A brand reporting only Scope 1 and 2 is, by definition, missing the vast majority of its actual climate impact.

The GHG Protocol's Scope 3 Standard divides Scope 3 into 15 categories across upstream and downstream activities.

The 15 Scope 3 categories

Upstream

1. Purchased goods and services: cradle-to-gate emissions of all purchased goods and services.

2. Capital goods: emissions from producing capital equipment.

3. Fuel and energy-related activities: emissions from producing fuels and energy not in Scope 1 or 2.

4. Upstream transport and distribution: transport of goods from suppliers to the company.

5. Waste generated in operations: emissions from disposal of operational waste.

6. Business travel: employee travel in non-company vehicles.

7. Employee commuting: employees travelling to and from work.

8. Upstream leased assets: emissions from leased assets not included in Scope 1.

Downstream

9. Downstream transport and distribution: transport of finished goods to retailers and consumers.

10. Processing of sold products: further processing of intermediate products by the buyer.

11. Use of sold products: emissions from consumers using the product.

12. End-of-life treatment of sold products: emissions from disposal and recycling of sold packaging and products.

13. Downstream leased assets: assets leased to others.

14. Franchises: emissions from franchised operations.

15. Investments: emissions from the company's investment portfolio.

Where packaging emissions sit

For most consumer goods brands, packaging emissions appear primarily in two Scope 3 categories.

Category 1: Purchased goods and services

This is the most significant category for packaging. Category 1 covers the cradle-to-gate emissions of everything a brand purchases, and all packaging materials fall here.

For food and beverage brands, packaging is often the largest or second-largest single contributor to Scope 3 Category 1. The carbon footprint of producing flexible film includes:

- Extraction and refining of the fossil fuel feedstock (oil or natural gas)

- Extrusion and conversion to produce the film

- Any printing, laminating, or further converting steps

All of this happens before the packaging ever reaches your facility, and all of it sits in your Scope 3.

Category 12: End-of-life treatment of sold products

Category 12 covers the emissions associated with how your packaging is disposed of once consumers have used it. Packaging sent to landfill, incinerated, or processed through energy-from-waste facilities each carries a different carbon outcome. Packaging that is genuinely recycled has a lower Category 12 profile because recycling displaces some of the emissions that would otherwise come from producing virgin materials in future cycles.

For flexible plastic packaging, Category 12 currently reflects the reality that most flexible film goes to landfill or energy recovery rather than mechanical recycling. As recycling infrastructure improves, the Category 12 profile of recyclable flexible packaging will improve accordingly.

The transport connection

Category 9 (downstream transport and distribution) is directly influenced by packaging decisions. Heavier, bulkier packaging increases transport emissions per unit of product moved. Flexible packaging's weight advantage over glass and many rigid formats is a genuine carbon benefit that is often overlooked in conversations focused solely on recyclability.

When Scope 3 disclosure becomes mandatory

Scope 3 reporting has historically been voluntary. That is changing rapidly across multiple jurisdictions.

California SB 253 (the Climate Corporate Data Accountability Act), signed in 2023 and effective from 2026, requires companies with revenues above $1 billion that do business in California to disclose Scope 1, 2, and 3 emissions annually. California represents roughly 12% of the US population and the world's fifth-largest economy, meaning SB 253 has effectively set a national standard for large US companies.

The EU Corporate Sustainability Reporting Directive (CSRD) requires large EU companies and non-EU companies with significant EU operations to report material greenhouse gas emissions including Scope 3 under the European Sustainability Reporting Standards. Tens of thousands of companies are in scope, including many that sell packaged goods in European markets.

The GHG Protocol's Scope 3 Standard is currently being revised. A public consultation draft is expected mid-2026, with a final revised standard targeted for late 2027. The revision is expected to tighten data quality requirements, expand mandatory categories, and introduce standardised exclusion notation.

What this means for you and your brand

Your packaging is a Scope 3 emission for your brand and a Scope 1 or 2 emission for your packaging supplier. That asymmetry is why supplier engagement matters: reducing the embedded carbon in your packaging requires working with your supplier on the emissions in material production, not just measuring what arrives at your warehouse.

Brands that treat Scope 3 as a supply chain design challenge rather than a reporting task will be better positioned as disclosure requirements tighten. Retailers, investors, and increasingly consumers are asking for quantified emissions data at the product level. The brands that have already mapped their packaging footprint across Category 1 and Category 12 will have a meaningful advantage when those requests become requirements.

Frequently asked questions

Why does Scope 3 matter if my brand does not manufacture anything directly?

Scope 3 matters precisely because the emissions associated with your brand's activity happen outside your direct operations. A brand that designs and markets a packaged consumer product but outsources manufacturing, packaging production, and logistics still has a large emissions footprint. It is just invisible in Scope 1 and 2. The full carbon impact of producing your packaging, making your product, transporting it to consumers, and disposing of it after use is Scope 3. Regulators, retailers, and investors increasingly require companies to account for and reduce this full footprint, regardless of whether they directly operate the emitting activities.

What is the difference between Scope 3 Category 1 and a product carbon footprint?

Scope 3 Category 1 is a corporate accounting category covering the cradle-to-gate emissions of everything a company purchases, including all packaging. A product carbon footprint (PCF) covers the full lifecycle of a specific product from raw material extraction through manufacturing, use, and end-of-life. Category 1 is how you account for packaging emissions at the company level; a PCF is the product-level measurement. A lifecycle assessment (LCA) is the methodology used to produce a product carbon footprint.

Does switching to recycled content flexible packaging reduce my Scope 3 emissions?

Yes, typically. Post-consumer recycled (PCR) flexible film generally has lower Scope 3 Category 1 emissions than virgin film because the energy-intensive raw material extraction and polymerisation steps are replaced by lower-energy mechanical recycling processes. The exact reduction depends on the recycled content percentage, the recycling technology, and the energy mix at the recycling facility. Studies consistently show that higher recycled content reduces the cradle-to-gate carbon footprint of flexible plastic packaging.

Other posts you may like:

Explore custom packaging solutions

Subscribe to our newsletter

Stay up to date with packaging news and industry updates.